4. Mid-Cap and Small-Cap Stocks Will Lead The Market. Mid-cap and small-cap stocks are still in the process of recovering from their five years of underperformance from 1994-1999 (chart, opposite page). Mid- and small-cap indexes have already hit new highs in terms of relative strength, but since their best performance usually occurs later in an economic recovery, as investor confidence builds up more and more, their best performance should be still ahead of us. (Small growth stocks or small value stocks? Both look equally attractive here.)

5. Big NASDAQ Stocks Remain The Big Problem Area. Big NASDAQ stocks are in the process of correcting their recent excesses, but history tells us that the process is likely to take a lot more time to be completed (big growth stocks, for example, generally went nowhere for a full decade following their 1972-73 peak). There will undoubtedly be a few big winners in the big NASDAQ stock area this year, but investors should realize that the odds are very much against them in this area of the market. It is also worth noting that while the NASDAQ 100 fell 32.6% last year the much more broadly-based NASDAQ Industrial index was off only 6.3%; the problem area is thus not NASDAQ stocks in general but, rather, the big NASDAQ stocks.

THE MARKET NOW. Turn-of-a-year cross-currents traditionally dominate trading in last December and early January, and this year has been no exception. We're thus waiting for the cross-currents to dissipate before we try sinking our teeth into the market's current numbers. One thing to watch, though: a month ago, there were 162 new highs on the NYSE and 142 on NASDAQ, and those numbers have not been bettered since then. If they were to be, it would indicate that participation in the current rally is broadening out significantly, and that the rally is thus more than a run-of-the-mill advance.

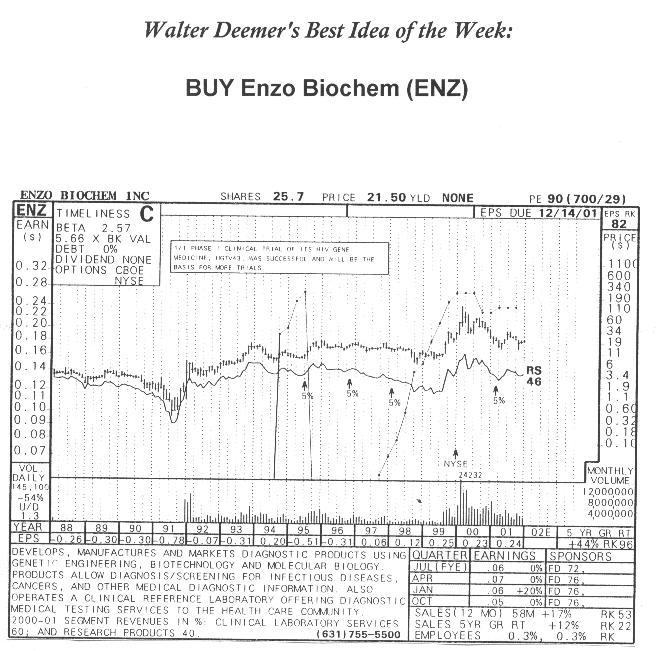

BEST IDEA OF THE WEEK. Enzo Biochem has just joined Techne as the only biotech stocks ranked "1" by Value Line. Since we think that biotech stocks represent the most attractive part of the NASDAQ-type (aggressive growth) area of the market, Enzo becomes our Best Idea Of The Week this week.

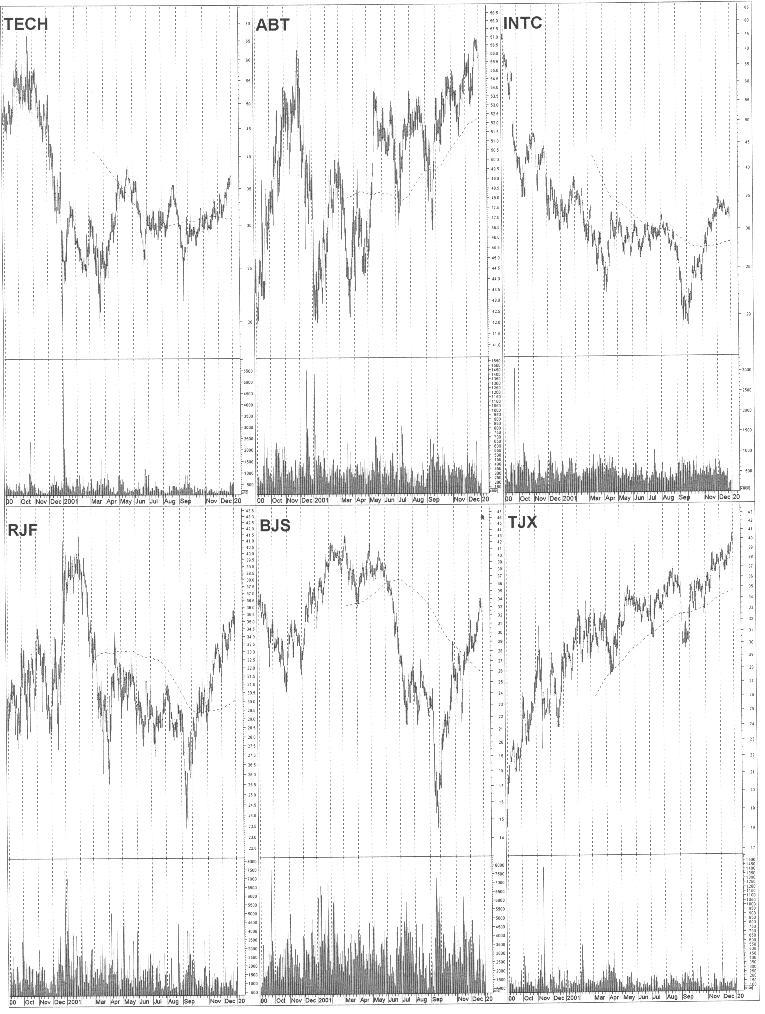

STOCK COMMENTS. As just noted, Techne is one of the only two biotech stocks that currently sport a "1" ranking in Value Line; it looks VERY good technically. Pharmaceutical stocks, meanwhile, look pretty good as a group; Abbott is the current leader there. As far as big NASDAQ stocks are concerned, though, the odds are against investors at this point, but, as always, there are a few exceptions; Intel is one, along with Dell and eBay. This is the time in the market cycle, meanwhile, when financial stocks should do well; regional banks and brokers look a lot better than their big brothers do. Energy service stocks, in the meantime, have been under a lot of pressure recently, but BJ Services is in a lot better shape than most (and thus in good position to lead the eventual recovery there). And, finally, retail stocks have been strong of late, as the chart of TJX demonstrates; retailers, though, are usually early movers in a market recovery cycle, so it may be getting a bit late in the game to build substantial new positions in them.

NOTED WITHOUT FURTHER COMMENT. Effective as of January 1, 2002, Blanchard and Company [the outfit started by Jim Blanchard that lived, breathed, and swore by gold] is changing its business practices and policies in order to limit its exposure to falling gold prices, and is recommending to its clients that they do the same. "As of that date Blanchard will not maintain inventories of gold bullion or gold bullion products, nor will it market gold to, or solicit gold sales to, Blanchard clients."

OUR OWN MONEY remains fully invested. Our portfolio is split evenly between mid-cap stocks (half in Kayne Anderson Rudnick Small Mid Cap, KASMX, and half in Vanguard Selected Value, VASVX) and small-cap stocks (half in Perkins Opportunity Fund, POFDX, a small small-cap growth fund, and half in Third Avenue Value, TAVFX, a small-cap value fund) - which means it is also split evenly between growth and value stocks. Our Fidelity Select money, meanwhile, is also 100% invested, split evenly between the Biotechnology, Home Finance and Industrial Materials funds. Last year, meanwhile, we almost made it; our portfolio was only off .2%. This is a heck of a lot better than the S&P's 13% decline, but every money market fund in America did better that we did last year, so the victory is tainted at best - and as I noted last year, relative performance in a down market sucks. Our Fidelity sector fund portfolio, meanwhile, was off 6.8% last year -- better than the S&P but a lot worse than cash. Things, I suppose, could have been a lot worse, but my money management "skills" left something to be desired in 2001.

THE BOND MARKET, following a horrendous decline, appears to have gone into a very wide-swinging trading range. At this stage of the economic cycle, though, its recovery potential is probably pretty limited, and we much prefer stocks to bonds here.

BEST AND WORST GROUPS. Charts of the four best and worst-performing groups during the last seven weeks may be found, as usual, in the back of the report. To supplement those lists: Waste Management and Trucks & Parts rose onto the top four list for the first time this week, while Semiconductors and Electronics-Instrumentation fell off; meanwhile, Electronic Defense fell onto the worst-performing list this week while Oil & Gas Exploration & Production resurrected.

OUR FIDELITY SECTOR FUND relative strength work was unchanged this week; no funds rose above nor fell below the money market rate of return. This left the percentage of funds outperforming cash at an impressive 88%; although this is well into overbought territory (above 66%), the percentage can stay overbought for a long time before it finally drops below 66% and triggers a "sell signal". Alas; the Biotechnology fund, one of the "holdings" in our switching program, triggered two of our sell criteria this week. The fund will therefore be sold and the proceeds reinvested in the highest-ranking fund not already owned: Software. We should note, however, that we think the weakness in the Biotech fund's strength rating is due to the fund's volatility (plus, perhaps, the turn-of-the year cross-currents in the market) rather than any significant longer-term deterioration. We still think the biotech group is a very attractive group from a longer-term technical standpoint, and neither our enthusiasm towards the group nor our "own money" position in the Biotech fund is being reduced here. The other two holdings in our switching program, meanwhile, are unchanged from a week ago: the #4 Electronics fund and #18 Gold.

THE MAJOR OVERSEAS MARKETS are, like our own, in recovery modes. The German market is significantly stronger than the U. K. market, and thus remains our market of choice if you want some overseas exposure. The Japanese market, meanwhile, is trailing behind the other major markets of the world, and we would wait for more of a bottom to develop before doing much buying there.

Walter Deemer