LEADERSHIP: OUT WITH THE OLD --

BUT WHERE IS THE NEW?

SUMMARY AND CONCLUSIONS. The longer-term indicators still look pretty ominous at this point, and the answer to the big question where the new leadership is -- remains very much in doubt. Caution is therefore still advised.

THE MARKET NOW. The longer-term indicators still look pretty ominous at this point. Among them: The market is still fighting the Fed, and the monetary indicators are still negative as well. (The 13-week annualized rate-of-change of M3 -- Ed Hyman's chart, not shown -- peaked at 16.6% in late December, fell to 5.0% in early April, struggled back to 7.4% in May, but has now slipped back to 6.5%.) In addition, Fidelity's sector fund cash/asset ratio is currently 2.3% just .3% above its March all-time low indicating that most of the (meager) cash that was raised during the April selloff has now been put back into the market WITHOUT enabling the NASDAQ (which is where by far most of the select assets are deployed) to recover anywhere near its old high. Our "normalized" NASDAQ/NYSE volume ratio, at 1.06, is also much too high to indicate a significant bottom in that area of the market. Add to this the fact that we are still in the midst of the generally-lackluster May-October timeframe and the fact that although the stock market in general is trying very hard to look over the Fed-tightening valley, individual stocks particularly in the key financial area are still getting hit hard on bad news and the result is a rather ominous-looking long-term picture.

From a very short-term standpoint, though, things look a bit brighter. The beginning of a new quarter tends to be "seasonally strong" due to the funding of retirement plans, and the July quarter is just about the strongest of all (probably due to the thinness of the markets at that time of year; in fact, the day before the Fourth Of July, statistically, is the most likely day of the year for the market to advance). That "seasonal strength" will have dissipated by the time the first week of July is out, however, and given yesterday's market weakness it will be very difficult for the averages to reverse the negative implications of last week's breakdowns in the Dow and the S&P by then. The stock market is therefore likely to end up in a very vulnerable position once the beginning-of-a-quarter seasonal strength dissipates, especially if volume remains on the light side during any rallies, and caution is therefore advised.

LEADERSHIP: OUT WITH THE OLD BUT WHERE IS THE NEW? Each passing day makes it clearer and clearer that the old leadership, the big technology stocks, are no longer leading the market (more on this in Stock Comments) -- just as the Standard and Poor's folks are adding more and more of them to their index. The big question, though, is where the new leadership is; so far, the answer remains very much in doubt.

Small vs. Big. The choice here seems pretty obvious, given the huge exploitation of big, aggressive growth stocks during the past couple of years which is now unwinding and the concurrent underperformance of small stocks. The market, though, is not in any particular hurry to embrace small stocks. The Perkins Opportunity Fund, our proxy for small-cap growth stocks, was at 14, for example, when we bought it last November, and subsequently went all the way up to 28. After that, though, it fell back to 18, and has only managed to struggle back to 20« since then -- which is hardly the performance we would expect to be seeing if small growth stocks are the new market leaders. (Contrast the fund's recent performance with its steady rise late last year and early this year; the symbol is POFDX if you want to look at it yourself.) Small growth stocks, in other words, SHOULD be market leaders but they are not acting like it yet.

Growth vs. Value. Here, too, given the exploitation of growth stocks and the long, long period of underperformance by value stocks, the choice seems fairly obvious. Our basic industrial (or commodity cyclical) average, though, is about a hard-core value area of the market as you can get and it is acting just horribly both from a short-term and a longer-term standpoint, as you can see from the chart in the back of the report. From a long-term basis, then, value stocks SHOULD also be market leaders, but they, too, are not acting like it yet.

And so what DO we have as market leadership? A few a very few of the last remaining survivors in the big technology stock area; they are fighting a strong outgoing tide, though, and their numbers are likely to dwindle still further as time goes by. More promising are the big consumer growth stocks, which have already been beaten-down and are now, in at least some cases, staging strong rallies. The unhappy conclusion, however, is that although we realize that the question of where to invest is uppermost in everyone's mind, the answers are still very unclear at this point.

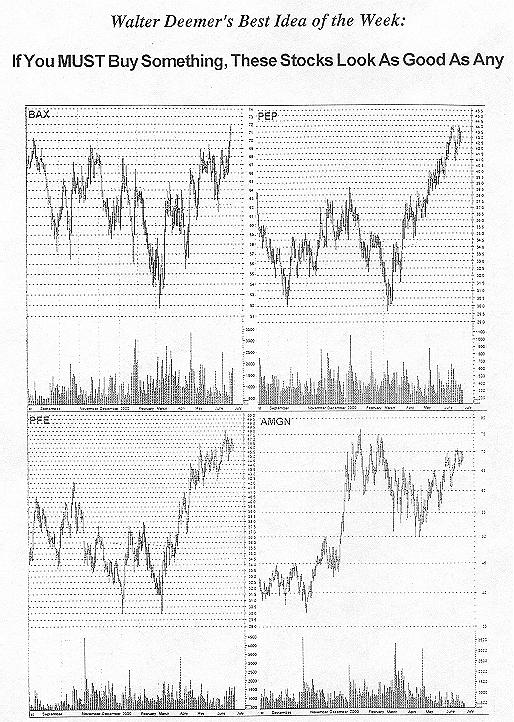

BEST IDEA OF THE WEEK. In view of the foregoing on both the general market situation and the leadership one, we are not particularly enthusiastic about buying anything here. If you HAVE to buy something, though, previously beaten-down big consumer growth stocks like Baxter, PepsiCo and Pfizer look as good as anything here. But if you have strong fundamental conviction in a big beaten-down consumer growth stock that has NOT enjoyed much of a recovery yet, buy it; it will probably do even better than our names as investors rediscover it. We've also included one of the (few) big aggressive outliers, Amgen, just to show that there are at least a few decent-looking stocks in that beleaguered area of the market (it also helps that biotech stocks tend to move ahead of aggressive stocks in general).

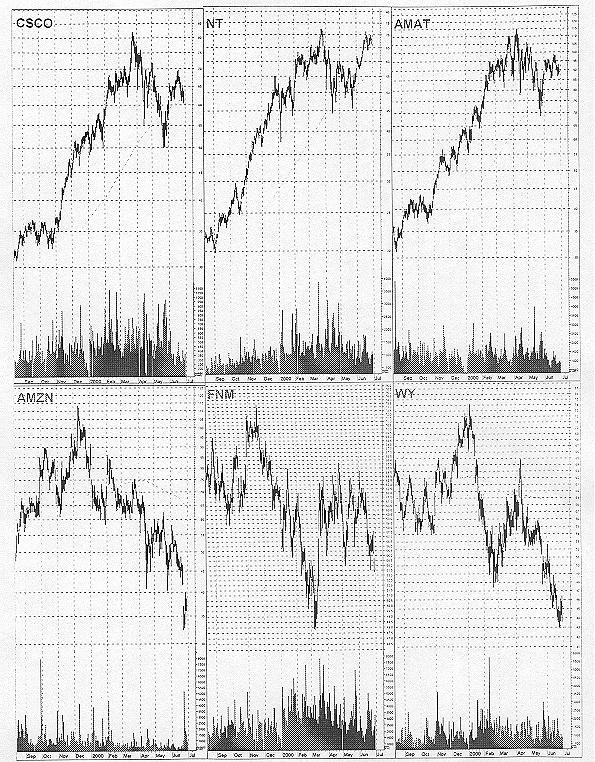

STOCK COMMENTS. It is becoming clearer and clearer with each passing day that the back of the big speculative advance in technology stocks has been broken, and even the creme de la creme technology stocks, such as Cisco, are generally on the defensive here. Generally, once the back of a big advance has been broken, the creme de la creme stocks evolve into big wide-swinging trading ranges (as McDonald's did in the 1970's and 1980's), and that probably represents a "best case" for most big tech stocks here. (Interestingly, Value Line downgraded Cisco, Qualcomm and Sun Microsystems from a "1" to a "2" ranking this week; while the historical difference in performance between their "1" and a "2" ranked stocks is not terribly great, the trend is, to say the least, an interesting one.) Historically, meanwhile, some of those creme de la creme stocks can get back to their old highs in the process of establishing their "big wide-swinging trading ranges", as Nortel has done and a VERY small number can even make minor new highs in the process. Fighting an outgoing tide, though, can be very difficult, and decent long-term performance in the group is likely to be very difficult to come by on anything other than a VERY selective basis. The semiconductor group, meanwhile, has been one of the strongest of the technology groups in the market during the past month or so, but many of the chip stocks are starting to look toppy and since the group is a laggard within the market, there are no longer-term positive implications for the general market stemming from that strength. Amazon, in the meantime, is a striking example of what can happen when a formerly-highly exploited stock fails in its attempts to establish a big, wide-swinging trading range, and the (still-evolving) Amazon chart thus represents the "worst case" for the creme de la creme stocks.

On another front, it looks like Fannie Mae, a bellwether financial stock, is failing to hold support in the 54-56 area, which has negative implications for the market as a whole. And, finally, the "value" area of the market is still having a terribly difficult time in finding a sustainable bottom as the chart of Weyerhauser a stock which is now selling for just 12 times earnings illustrates.

OUR OWN MONEY remains in a money market fund. Given the strength in some of the market's more aggressive areas during the past month or so, this has clearly not been the best place for it, but with the long-term picture as ominous as it is we think the risk/reward ratio in those "more aggressive areas of the market" is very unfavorable here -- and we can not find anyplace else to put it. We are thus perfectly content to stick with our money market fund here.

THE BOND MARKET looks like it is making some sort of top here. We think bonds will outperform stocks for a while, but their ability to outperform cash in the process is questionable.

BEST AND WORST GROUPS. Charts of the four best and worst-performing groups during the last seven weeks may be found, as usual, in the back of the report. To supplement those lists: Semiconductors rose onto the top four list for the first time this week while Savings & Loans fell off; meanwhile, Household Furniture & Appliances fell onto the worst-performing list this week while Building Materials resurrected. (The groups moving out of each category are probably the most timely to look at, since extreme strength or weakness is dissipating there; if you are able to anticipate such a move in one of the current top or bottom groups, though, it would be even more timely.)

OUR FIDELITY SECTOR FUND relative strength work deteriorated slightly this week as two funds, Leisure and Business Services, fell below the money market rate of return. This left the percentage of funds outperforming cash at a ever-so-slightly bullish 67%; the early-May "sell signal" was never reversed (the percentage fell only to neutral without getting oversold, then went back up again), and the percentage is now back in bullish territory again. (The percentage, however, would only have to drop slightly, to below 65%, to generate another "sell signal".) Meanwhile, the holdings in our switching program are unchanged from last time: the #2-ranked Electronics fund, #11 Energy Services and #16 Airlines.

MAJOR OVERSEAS MARKETS. Not much change since last time; the DAX is still entrenched in a solid long-term uptrend, and the FTSE still looks VERY toppy. The Nikkei, meanwhile, staged too much of a decline for comfort during April and May, but has been stabilizing nicely in the 16000-17500 area which should ultimately set the stage for another good advance in Tokyo.

-- Walter Deemer