THE BIG PICTURE

SUMMARY AND CONCLUSIONS. Stocks are in the midst of an emotional, news-driven decline that could end at any time, and our long-term working premises are still pretty much the same despite the selloff.

OUR LONG-TERM WORKING PREMISES, as presented in our September 7th report, require surprisingly little revision in the aftermath of this week's selloff, indicating that the selloff is an evolutionary, not a revolutionary event. Our September 7th premises are reprinted in italics, and are followed by our current thoughts.

6. The basic underlying consideration for the next 5-10 years, for investors and money managers alike: Average returns in the stock market will be a lot less than they were during the last seventeen years as it "reverts to the mean".

We moved this to the top spot because it is the REAL biggie for investors now. The stock market has been showing signs of a secular transition (from bull to something else) for several years now, and recent events (which have done things like eliminate the peace dividend and the Federal budged surpluses) only underscore the fact that the secular bull market is, indeed, a thing of the past, and has been replaced by something else.

It may be a long time, though, before we know exactly what that "something else" is. Investors and money managers alike, however, are going to have to get used to the idea that total returns in the stock market are, indeed, going to be a lot less for the next 5-10 years than they were during the last 17 as the stock market "reverts to the mean". This does NOT, however, mean it is going to revert in one fell swoop; history, rather, suggests that the reversion is more likely to be a long, slow process that takes the averages more sideways than down. This, in turn, suggests that a selective, sector by sector and group by group approach to stocks is now much more likely to generate above-average returns than a broadly-based one (although we still think that mid-cap and small-cap stocks in general will outperform large-cap stocks). It also suggests that if the market evolves into a broad "trading range" market, a la the 1970's, investors who have forsaken "market timing" are going to have to rethink their decision.

But -- this is NOT the time to start saying "secular bear market"; "secular flat market" is probably a much more appropriate label. The sector charts in the back of the report, for example, are all, with but one exception, still comfortably above their 1998 lows - and thus remain in secular uptrend. That one exception: the NASDAQ, where new highs are out of the question for a long time to come (if the NASDAQ rises at a compounded 8%/year rate, it would be fifteen years before it got back to its old high - and an 8%/year return on equities at this point appears to be an overly generous assumption). We therefore reiterate our point #5:

5. The stock market is not in a secular bear market (just the NASDAQ).

As for our other working assumptions:

1. The stock market has completed a

cyclical bear market and now in a basing process (which, as usual, has involved

tests of the prior lows; one of which is taking place now). A new bull market

has thus begun - but not yet in full force.

Wrong. The "test of the prior low"

turned into a new leg down - and given its force, we think it would have done so

even without the terrorist attack. We have no excuses...

2. The stock market is

close enough to the economic trough (within 6 months) to have made [make] a

major bottom. It is also now close enough to the economic trough (within 2-3

months) where it could complete its basing process at any time.

Still valid. ISI is now looking for real GDP to decline at least 2.0% in the fourth quarter, then gain 2.5% in 2002's first quarter. This suggests that the bottom will either be late in the fourth quarter or part way through the first - which means that the broad and powerful advance that heralds a new bull market, and which precedes the economic trough by 2-3 months, should begin late in the third quarter or part way through the fourth.

3. The fact that the bull market has gotten underway in earnest should be heralded by an unusually powerful advance (one that generates "breakaway momentum"; advances more than 1.97 times declines over a ten-day period).

In view of the most recent decline, this is practically a given now.

4. Leadership in this bull market will not be the same as it was in the last one -- and will also be a lot more selective than usual (see #6). The main thrust of leadership will be in the mid-cap and small-cap areas of the market (with both growth and value stocks participating).

We see no reason or need to change this at the present time.

The bottom line: Stock market returns are likely to be below normal for many years. Well-selected stock market investments should generate above-average returns, but stocks in general will not. In addition, market timing will be much more important in the future than it was during the now-ended secular bull market.

THE MARKET NOW. Two weeks ago, I wrote: "The current decline - especially in tech stocks - has been disturbingly strong. Is the decline trying to tell us something; is the short-term picture so bleak that it's overriding the long-term positives?" After reporting on the soul-searching that I had done, I concluded: "I am going to go with my bullish long-term indicators, and am NOT going to let the market's short-term gyrations distract me from its very bullish long-term message."

This was a huge mistake. The decline WAS trying to tell us something - and given the magnitude of this week's selloff, I think the market would have decisively broken its April lows no matter what happened. I am not, in other words, going to blame the market's tailspin (and my misreading of the indicators) on the terrorist attack; the selloff undoubtedly would not have been as violent otherwise, but the market WOULD have gone down anyway, and I simply underestimated the significance of the short-term warning signs.

So what will tell us that this violent and emotional decline has ended? Not oversold indicators; although the market is now oversold -- big-time -- there's simply no way of telling just how oversold it will finally get during this emotional and news-driven decline. The same holds true for the sentiment indicators; many of them, such as the put/call ratio, are already at extremes, but there's just no way of telling just how extreme the readings will get before we are through. Suffice it to say, though, that both short-term and long-term indicators in general are now in positions that have historically been associated with significant stock market bottoms.

What we really need to watch here, I think, are volume and price action. If volume increases dramatically, it would indicate that prices have declined to the point where buyers are being attracted to the market in a big way - and that would be very bullish. (The decline could also end with a whimper, not a bang, as sellers simply run out of stock to sell, but that appears to be pretty unlikely at this point.) The other thing to watch is price action itself; at some point, the thrusts on the downside will become less and less violent, and the trading rallies will retrace more and more of the decline that immediately preceded them, demonstrating that the downside momentum is starting to dissipate. Neither of these two things has happened yet - but they could obviously materialize very quickly when the time comes. (We need VERY strong breadth and upside/downside numbers, though, to indicate that the market is staging a good rally and not just a snapback one. And so we're left with an emotional and news-driven selloff taking place against a technical background that is equivalent to the technical background that existed at the end of previous emotional selloffs, but with a market that has shown no signs of reversing yet. Those "signs of reversing" are likely to appear very quickly when the time comes, though (perhaps even on an intraday basis), and we will keep you posted as events continue to unfold.

THE STOCK MARKET IN 1990-1991. The present situation is becoming more reminiscent of the market action following the invasion of Kuwait on August 2, 1990 than I would have liked. The chart on the back page shows what the market did back then. The S&P's initial reaction to the invasion (arrow on chart) was to sell off 5.9%; it then rallied 1.7% in six trading days, then sold off another 9.7% to its initial low on August 23rd. The initial leg down was 13.6%; the final low, in October, was 3.8% below that, making the total decline 17%. (If you were wondering, the current S&P equivalents would be 944 and 907 - although history is far from likely to repeat exactly.)

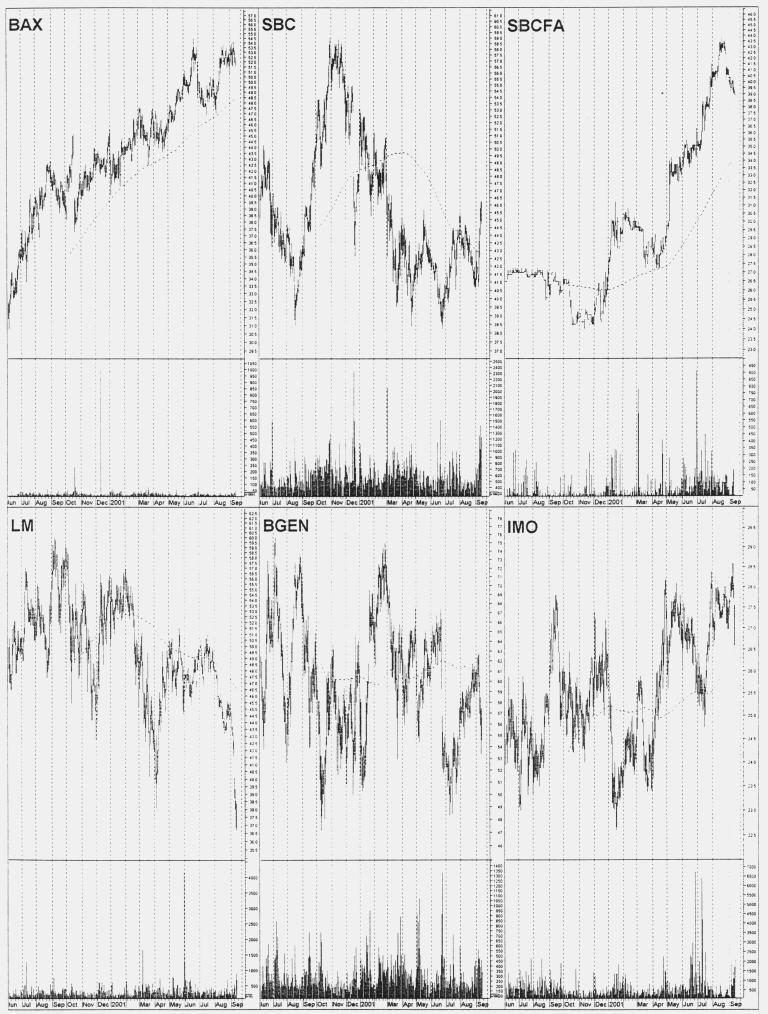

STOCK COMMENTS. Trying to accentuate the positive: Healthcare stocks, such as Baxter, have been relatively untouched by this week's selling; since they are traditional early movers in the market, their strength should persist into the early part of the next bull market. The old Bell Operating Companies, such as SBC, also look good here. Regional banks such as our local Seacoast, meanwhile, still look better than their money center counterparts, and the current market environment could create opportunities to buy otherwise-thinly traded stocks. Also, brokerage stocks have been decimated in the aftermath of the terrorist attacks, but should rally nicely "on the other side"; regional brokerage firms such as Legg Mason look more attractive than their big counterparts. In addition, we still think that the biotechnology group is a much better place to look for ideas than technology stocks in general. And, finally, energy stocks have been clobbered this week, but we suspect they will do better if America decides not to be so dependent on foreign oil. In any case, a few energy stocks, such as Imperial Oil, still look good amidst the carnage, and are probably as good a place to start looking as any.

THE BOND MARKET rallied to the area of its December 2000-March 2001 highs before reversing this week. The reversal was attributed to 1) Some asset allocators selling bonds to buy stocks and 2) A feeling among bond traders that the economic recovery might be stronger than many expect (obviously, they haven't been talking to their equity counterparts). Whatever the case, those old highs should help limit further upside potential in bonds, and we think the asset allocators are doing the right thing.

OUR OWN MONEY, unfortunately, was fully invested two weeks ago, and we were thus 100% patriotic going into the market's reopening. The money is split evenly between mid-cap stocks (half in Kayne Anderson Rudnick Small Mid Cap, KASMX, and half in Vanguard Selected Value, VASVX) and small-cap stocks (half in Perkins Opportunity Fund, POFDX, a small small-cap growth fund, and half in Third Avenue Value, TAVFX, a small-cap value fund.) This means that our own money is also evenly split between growth and value stocks. Our Fidelity Select money, meanwhile, is also 100% invested, split evenly between the Home Finance, Industrial Materials and Medical Delivery funds.

BEST AND WORST GROUPS. Charts of the four best and worst-performing groups during the seven weeks ending on September 5th may be found, as usual, in the back of the report. To supplement those lists: Containers-Metal & Glass rose onto the top four list for the first time this week while Oil-Domestic Integrated fell off; meanwhile, Consumer Finance fell onto the worst-performing list this week while Savings & Loans resurrected.

OUR FIDELITY SECTOR FUND relative strength work weakened still further this week as two more funds, Paper and Medical Delivery, fell below the market rate of return. This brought the percentage of funds outperforming cash down to 5%, which is in deeply-oversold territory, but it needs to rise above 33% to generate a new "buy signal". Unfortunately, Paper and Medical Delivery were two of the holdings in our switching program, and their fall below the money market rate of return triggered one of our sell criteria. The two funds will thus be sold; since only one fund not already owned, Gold, is currently ranked above the money market rate of return, our switching program will take a one-third position in Gold and put the remaining one-third into the money market fund. The third holding in our switching program is unchanged from a week ago: the #2 Food fund.

THE MAJOR OVERSEAS MARKETS have all broken their April lows, and are thus all in the same unhappy boat that ours is. (Interestingly, though, the long-beleaguered Japanese market is starting to show at least some tentative signs of relative strength, which will bear watching in the weeks ahead.

Walter Deemer