SUMMING UP OUR CURRENT

WORKING CONCLUSIONS

SUMMARY AND CONCLUSIONS. Seasonal pressures on the market should peak sometime during October; until then, though, discretion will remain the better part of valor. Periods of weakness should be used to buy the "new upside leadership", and periods of strength should be used to sell the "new downside leadership". This is also a good time to do fundamental research on mid-cap and small-cap companies and the depressed retailing and telecommunications groups.

SUMMING UP OUR CURRENT WORKING CONCLUSIONS.

1. The broad market averages should have a downward bias until we get closer to the end of the seasonally-weak September-October period.

We are currently seeing a bounce in response to the beginning-of-a-quarter funding of retirement plans, but the amount of weakness in September suggests that the final low is still ahead of us. Risks in the broad market averages, though, appear to be lessening both with the passage of time and improvement in things like the monetary indicators (top chart, next page).

2. Periods of weakness should be used to buy the "new upside leadership": the financial and utility groups (or at least the "non-energy" utility stocks), most drug and many big consumer growth stocks, and mid-cap stocks in general. (Small-cap stocks are trying to join the parade here.)

The stock market has become bifurcated. Many of the "new upside leadership" stocks made long-term tops as much as two years ago, then completed their bear markets last spring and are now in new bull markets. This makes them very attractive on a long-term basis.

The big question here: Is leadership spreading into small-cap stocks -- as we expect it to sooner or later?

3. This is a very good time to try to identify the most attractive mid-cap and small-cap stocks fundamentally.

These stocks are almost impossible to buy in size except during periods of market weakness, so you need to have your ducks lined up beforehand.

4. The big NASDAQ stocks that make up the "new downside leadership" still have a long way to go to finish correcting their past excesses, so we would resist any temptation to do any bottom fishing in them.

It takes time, as well as price weakness, to correct excesses of the magnitude we saw in big NASDAQ stocks earlier this year, and our NASDAQ/NYSE volume ratio (bottom chart) is nowhere near levels which would indicate that we are nearing a significant bottom. "When the time comes to buy Intel, you won't want to."

5. The energy sector is making some sort of top here.

This is traditionally the most laggard sector in the market. Everything ahead of it has already topped out on a rotational basis (and energy stocks usually move just after technology stocks, which topped out in March, do), so we'd use periods of strength to take some profits.

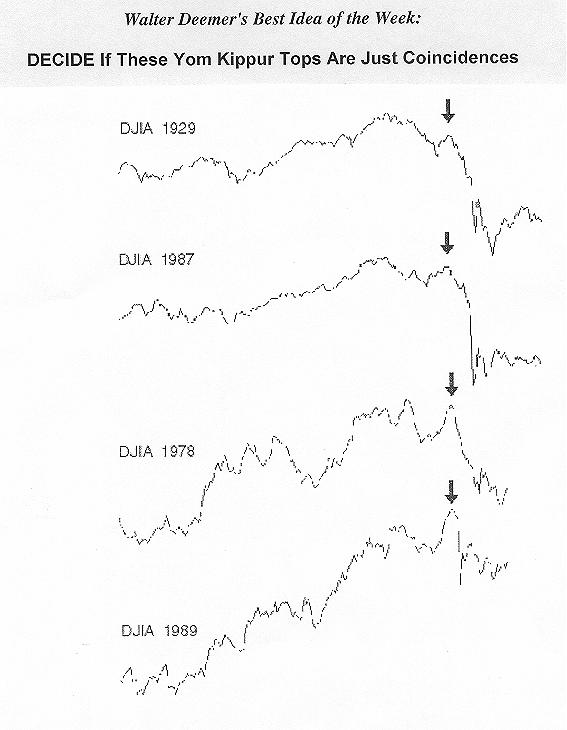

BEST IDEA OF THE WEEK. Chris Carolan shared the chart on the back page of the report with the MTA e-mail list this week, noting that "Yom Kippur [indicated by the arrows on the chart] has been the ideal shorting point in those years where markets have had October crashes."

Is this just a coincidence? If so, it's quite an amazing one -- and whatever the case, the week or two after October 9th should be very interesting ones for market-watchers. (Market "crashes", of course, are few and far between; if the market does happen to "crash" this October, though, we suspect it'll be the NASDAQ more than the whole "market".)

THE MARKET NOW. The market is traditionally buoyed by beginning-of-a-quarter inflows from funding of retirement plans, but the charts on the back page suggest that the September-October seasonal pressure, which has been a definite factor in September, is likely to peak during the second and third weeks of October. Discretion thus remains the better part of valor here.

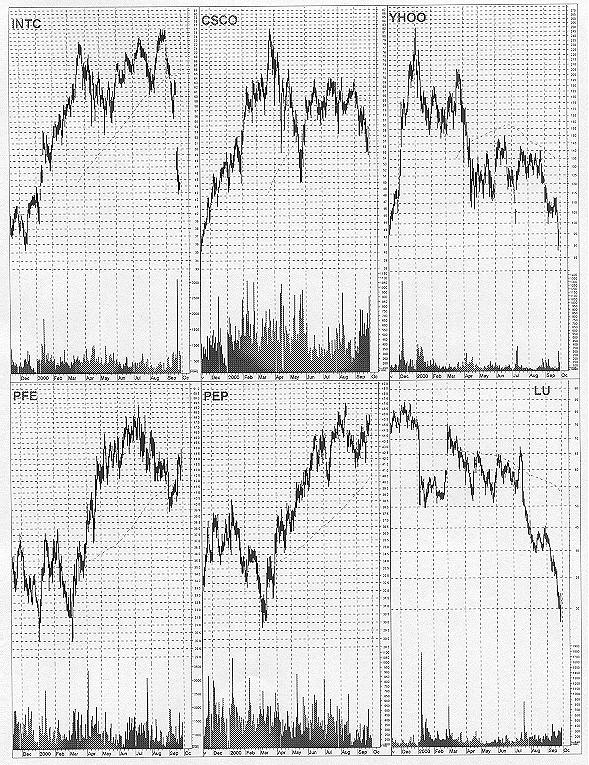

STOCK COMMENTS. The big story during the last five days was Intel; the stock plummeted following an earnings warning on Friday, and has been under pressure ever since. Intel, of course, is one of those big NASDAQ stocks that is providing the "new downside leadership" for the market, so was in the wrong place to begin with; we suspect that the stock will end up in a big trading range with a downward bias after it finds an initial bottom, but our comments about resisting the temptation to do any bottom fishing in big NASDAQ stocks very definitely apply to Intel. More ominously, Cisco which, along with Sun Microsystems, is probably THE key NASDAQ bellwether these days fell to a four-month low this week on no news at all (although the fact that the stock did manage to close up yesterday despite an analyst's downgrade indicates that the worst may be over for a while) and Yahoo broke its July low rather decisively this week. This all is further confirmation that big NASDAQ stocks are, indeed, the downside leadership here; they still have a long, long way to go, though, to finish correcting their past excesses, and we would therefore resist any temptation to do any bottom fishing in them. On the positive side of the ledger, meanwhile, most drug stocks and many big consumer growth stocks staged bear markets from 1998 or early 1999 until last spring, when they bottomed and embarked on new bull markets. This makes them very attractive on a long-term basis, and we thus consider any reactions in them as buying opportunities.

And a final note: The retail and telecommunications groups seem to be the most depressed and unloved groups among those that institutions have major holdings in. John Mendelson noted Tuesday that "mutual fund managers are told to complete their tax trades by [October 31]", and several portfolio managers in Boston told him "they have been told to minimize gains that were taken last spring." This suggests that if mutual fund "tax selling" does take place the retail and telecommunications groups could come under further pressure during the next month -- and could then bounce when it lifts. This thus looks like a good time to identify your favorite stocks in each group, just in case a buying opportunity does present itself in late October.

THE BOND MARKET is still stalled in the general area of its April high, and since bonds are currently underperforming interest-sensitive stocks, such as REITs and non-energy utilities, we would rather own interest-sensitive stocks than bonds here.

OUR OWN MONEY is still parked in a money market fund as we wait for the events of October to unfold. At this point, though, we suspect that we will be putting it back in the market sometime during the next month or two. The big question is where; do we put it in mid-cap stocks, which are already leading the market, or in small-caps, which have been lagging somewhat and thus have some catch-up potential (and which we think will almost certainly join the leadership parade sooner or later)? We suspect the answer may be "both"; stay tuned...

BEST AND WORST GROUPS. Charts of the four best and worst-performing groups during the last seven weeks may be found, as usual, in the back of the report. To supplement those lists: Oil & Gas Exploration & Production rose onto the top four list for the first time this week while Utilities-Electric fell off; meanwhile, Wireless Telecommunications, Aluminum and Containers-Metal & Glass fell onto the worst-performing list this week, while Drugs, Footware and Beverages-Non Alcoholic resurrected. (The groups moving out of each category are probably the most timely to look at, since extreme strength or weakness is dissipating there; if you are able to anticipate such a move in one of the current top or bottom groups, though, it would be even more timely.)

OUR FIDELITY SECTOR FUND relative strength work weakened a bit on balance this week as one fund, Business Services, rose above the money market rate of return but five others (Electronics, Technology, Computers, Developing Communications and Construction & Housing) fell back below it. This all brought the percentage of funds outperforming cash back down to 56%; the percentage thus continues to waffle back and forth between neutral and mildly-overbought territory without ever falling into fully-oversold territory, below 33%, which is what it would take to set up a full-fledged "buy signal". The holdings in our switching program, meanwhile, are unchanged from a week ago: the #5 Airlines fund, #8 Brokerage/Investment Management fund, and #15 Energy Services.

MAJOR OVERSEAS MARKETS. No big changes. The FTSE, after rallying to an eight-month high a month ago, decided it didn't like heights and has fallen back into its long-term "go-nowhere" pattern. The DAX has also declined, but looks much better than the FTSE longer-term. The Nikkei, finally, is still marching to the beat of a different drummer; as of this writing, it has bent but not decisively broken support just below 16000, but it needs to stabilize longer-term before we get excited about its long-term recovery potential again.

-- Walter Deemer